Why KYC Compliance is Crucial for Faster Merchant Onboarding

The merchant onboarding process sits at the crux of the payments segment, its efficacy the basis for or deterrent of growth for organizations in this soon-to-be $2-trillion industry. Rapidly evolving, the global payments industry faces challenges and opportunities brought on by regulatory changes, macroeconomic trends, and fintech’s foray into the payments business.

As payments organizations navigate the circumstances of the industry none are immune from the digital transformation that is sweeping financial services as a whole. Customers and merchants grow accustomed to speedier, more convenient service, turning payments providers to digital infrastructure improvements to gain advantages in speed and flexibility. Meanwhile, up and coming startups are bursting onto the scene with unprecedented agility.

“The transformation and disruption of the merchant services business is playing out right in front of our eyes – and in real time. I would characterize it as co-opetition on steroids right now as hardware, software, payments, processing services and new platforms all converge, consolidate and collide to reshape the merchant services supply chain in entirely new ways.”

– Karen Webster, President of PYMNTS.com

Merchant Onboarding: Key Topics

This guide to faster merchant onboarding explores foundational themes within merchant onboarding while offering the resources to dive deeper into topics of interest such as:

- Winning at Merchant Acquisition

- The Merchant Onboarding Process

- KYC Compliance

- Transaction Monitoring

- Merchant Onboarding Solutions

Winning at Merchant Acquisition

Merchant acquisition is plagued by the same age-old challenges around regulations, trends, and competition that reflect the payments industry at large. However, where the industry dynamic once danced between the competitive margins negotiated by large retailers and the compliance headaches brought on by smaller merchants, the spectrum has spread to include the burgeoning marketplace economy. This is a world where everyone is a merchant, rendering merchant onboarding volume and transactional volume simultaneously opportunistic and challenging. A segment of innovative payments firms is navigating the risk and compliance gap that the marketplace economy has introduced.

As the payments industry evolves to serve ever growing commercial channels, organizations strive to improve around two major advantages: speed and compliance.

Some of the biggest disruptors in the payments segment have excelled with five-minute onboarding times in the face of an industry that traditionally accepted a 3-5 day, even up to weeks-long, merchant onboarding process. Shrinking onboarding cycles that automate compliance coupled with advanced analytical capabilities are contributing to simpler-than-ever merchant experience as processors and facilitators are able to handle the astounding volume.

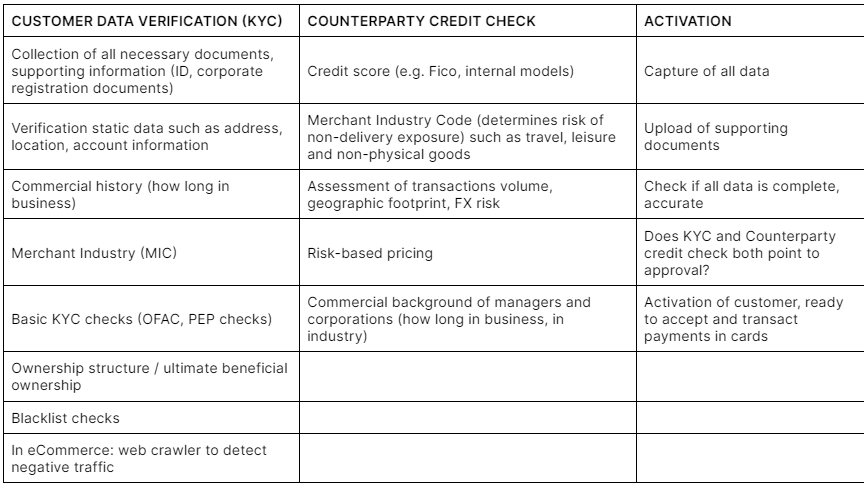

KYC Compliance

The nature of each transaction and associated risk will determine its responsibility with regard to various global KYC statutes. For example, payments facilitators face regulatory requirements on either side of the decoupled transaction. They are subject to regulations as they charge customers, and again when they disburse funds to merchants. In some scenarios, payments providers are assuming additional risk on behalf of merchants and so KYC processes are integrated into complex credit risk workflows. Intricacy only increases when companies are engaging in cross-border activity or operating in particularly regulated industries.

While the KYC/AML component of the merchant onboarding process used to be highly manual, today’s foremost payments firms are adopting advanced automation technologies to support:

- The integration and standardization of structured and unstructured data in support of OFAC and PEP checks, blacklist checks, and other due diligence resources.

- Business rules and process workflows that automate cross-border or regional specialization, intelligently applying appropriate rules to ensure compliance in every case.

- Implementation of traditional and machine learning techniques in the creation and native operationalization of analytical models.

Transaction Monitoring AML

Like every corner of the payments universe, transaction monitoring and AML/CFT compliance are being propelled forward by technological progression. In fact, three movements have most significantly impacted AML/CFT monitoring:

- Proliferation and accessibility of data.

- Enhanced processing power that supports unprecedented speed and volume.

- Widespread acceptance of advanced data analysis techniques.

Proliferation and Accessibility of Data

Historically, AML exposure data has been centralized to a select group of firms – packaged and commercialized for global use. However, around the time we gained the ‘Big Data’ buzzword, payments firms gained accessibility to a whole slew of untapped data. Pair the variety and volume of data that has become available with enhanced analytical capabilities, and compliance professionals now hold the reigns when it comes to powerful, data-centric AML/CFT insight.

In this era of automation, transaction monitoring strategies have to acknowledge the need for efficient data aggregation — the ability to analyze data is no longer enough. Web crawling technologies and copious APIs have opened up the world of data, and forward-thinking companies are capitalizing on its availability.

“Data! Data! Data! … I can’t make bricks with clay!

Sir Arthur Conan Doyle, Adventures of Sherlock Holmes

Enhanced Processing Power

In the meta-story, processing power has seen exponential uplift since the day we put an abacus in a museum. Let’s be precise: We have seen a 1-trillionfold increase in processing power over the course of 60 years.

In parallel to improved computing performance, we have also experienced a shift from primarily bare metal environments to cloud or hybrid infrastructures which introduce new opportunities.

Widespread Acceptance of Advanced Data Analysis Techniques

Machine learning is the future. Machine learning is here. It’s everywhere and for good reason. But, it’s not new. Machine learning in theory and application has a long history in academia and computer science. Now, it’s making its way into the mainstream of, well, everything – financial services notwithstanding.

Payments firms are familiar with machine learning techniques in transaction monitoring and data sciences are only becoming more predictive with time. Many firms are exploring ensemble models like Random Forest and Gradient Boosting to increase stability and accuracy in predictive analytics.

Merchant Onboarding Solutions

Provenir’s unified risk analytics and decisioning Platform can automatically gather data from multiple systems and bureaus, standardize and analyze it to drive a decision. With Provenir, you can complete KYC, AML and other compliance processes in minutes, offering clients quick onboarding while improving compliance at lower cost.

- Easily configured adapters facilitate fast integration with internal and external systems and bureaus to automatically aggregate all of the data required.

- Dynamic business rules ensure only the right data is aggregated, eliminating expensive, unnecessary calls to bureaus and third-party systems.

- Automated standardization creates data uniformity across multiple data formats, countries and currencies.

- Automated workflow identifies, verifies and validates the customer, performs checks and flags areas of potential risk.

- Adapters extend the value of current compliance systems as you can easily use Provenir to aggregate, standardize and pass data to existing systems.

- Business-friendly configuration tools let users quickly create, test, modify and deploy rules, processes, user interfaces and integrations to increase business-level control and agility.