Blog: The Importance of Customer Experience in Driving Loyalty Across the Subscriber Lifecycle

Telcos: The Importance of Customer Experience in Driving Loyalty Across the Subscriber Lifecycle

For telcos, delivering exceptional customer experience is more critical than ever. As service offerings become increasingly commoditized (and competition flourishes), telco providers have to differentiate themselves to stay ahead of the curve. And one of the best ways to do that? Create meaningful, frictionless interactions at every subscriber touchpoint across the journey. A seamless, well-crafted subscriber experience enhances customer satisfaction, sure. But the implications are more far reaching than that, playing a critical role in reducing churn, increasing loyalty, and maximizing the lifetime value of each of your subscribers. From the second a customer is onboarded, through to ongoing customer management (and collections treatments if it comes to that), optimizing the customer experience is crucial to maintaining long-term relationships and staying ahead of the competition. How can you elevate the experiences of your subscribers? Intelligent, holistic risk decisioning.

The Onboarding Challenge:

Onboarding in the telco industry is a complex process, in part because of the diverse needs of your customers, which can range from individual subscribers with little to no credit histories to large enterprises. Traditional (aka manual) onboarding methods often create bottlenecks, with lengthy wait times and inconsistent experiences – leading to customer frustration and increasing the risk of churn. And then there is the demand for real-time decisions, including credit assessments and fraud checks, which have to be handled quickly (and accurately) to keep up with increasingly high customer expectations. As a result, telcos are turning to automation to deliver a more seamless onboarding experience.

Enhancing Subscriber Experience:

Automation is changing the onboarding process, streamlining key steps that previously bogged down telco providers. One of the most impactful uses of automation is identity verification, which is a must-have step in every subscriber’s journey. Automated IDV tools can quickly and accurately collect customer data, reducing the need for manual paperwork that slows down the verification process. This speeds up onboarding of course, but also greatly enhances the accuracy of customer profiles, helping to ensure better service delivery right from the start.

Another key aspect is real-time credit risk assessment. Automated systems can enable you to instantly evaluate a potential subscriber’s creditworthiness, delivering immediate decisions that eliminate manual reviews – and the long wait times that are associated with them. This allows for lightning-fast onboarding and minimal disruptions for your subscribers, while still ensuring informed risk decisions.

Reducing Friction and Preventing Fraud:

Fraud is especially rampant in the telco industry. Last year, telco fraud increased 12%, worth an additional $38.95 billion lost. As a provider, you have to balance the need for speed in onboarding, while effectively detecting and preventing fraudulent activities. AI-driven automation in your risk decisioning can play a pivotal role – minimizing friction for your legitimate customers and ensuring robust fraud prevention measures for those that aren’t. Intelligent fraud decisioning can analyze multiple data points in real-time to detect and prevent fraud before it happens, without causing delays or unnecessary hurdles for your honest subscribers. Reducing that friction enhances the customer experience, and reduces the likelihood of false positives, which can frustrate potential subscribers.

When we’re talking fraud or other risk assessments, data integration is critical to creating a consistent, seamless onboarding experience across all channels. Whether your subscribers begin their journey online, in-store, or via a mobile app, automation in your data and decisioning processes ensures that all relevant data is collected and integrated appropriately. This level of orchestration and integration helps you provide a unified, personalized experience that results in an effortless onboarding experience in the eyes of your subscribers. And happy subscribers = long-lasting customers.

Personalized Risk Decisioning:

Your subscribers expert more than one-size-fits-all solutions, especially when it comes to financial decisions like credit approvals. For telcos, personalized decisioning will help manage your risk, but it’s also an opportunity to improve the satisfaction of your subscribers and build brand loyalty. Using real-time data to customize risk decisions based on individual profiles will allow you to offer a range of tailored options (including specific credit limits or repayment terms) that cater to each subscriber’s unique needs. Have high-risk customers? You can offer more cautious lending terms. Lower-risk subscribers? Give them higher credit limits or faster approvals. When individual financial situations are understood and accommodated, satisfaction and loyalty increase as a result.

Building Loyalty with Flexible Financial Solutions:

By offering more flexibility in your financial products, including personalized pricing and payment plans, you’ll further enhance the subscriber experience. You can leverage subscriber history and credit profiles to provide tailored pricing that matches a customer’s financial capacity, preferences, and risk tolerance. This kind of flexibility fosters a sense of fairness and transparency, building trust in your brand. But clear communication is essential in this process. When you provide your customers with choices (repayment terms, plan upgrades, credit extensions), you empower subscribers to make informed financial decisions that best suit their unique circumstances. This transparency strengthens relationships long-term – and these days, with the extreme proliferation of competition, you can never have too much brand loyalty.

The Role of AI/ML in Intelligent Risk Assessment:

Offering flexible, personalized options is easier said than done. That kind of agility requires advanced technology, including intelligent decisioning with AI/ML capabilities. By analyzing vast amounts of customer data, AI-driven risk decisioning technology can quickly and accurately assess the creditworthiness of your subscribers, making real-time decisions possible across the subscriber lifecycle. With the use of machine learning algorithms, you can refine your risk assessments over time, continuously enabling smarter and more efficient risk decisions and more easily identifying patterns that point to fraudulent activities or the need for financial support. The use of AI not only makes your risk assessments faster, but it helps create a strong foundation for sustainable subscriber growth. Faster, smarter risk assessments = the ability to better manage your risk and offer personalized products to your loyal customers. An intelligent, data-driven approach to decisioning ultimately means a more satisfying customer experience and a more nuanced risk strategy for long-term growth.

A memorable (in a good way!) customer experience goes beyond onboarding – it extends to the ongoing management of risk and fraud across the entire subscriber lifecycle. With continuous monitoring for fraud and credit risk, you can stay ahead of potential issues without disrupting the customer experience – and actually help to improve it. With advanced analytics and AI-driven tools, you can identify and address risky behaviors or anomalies in real-time, ensuring your customers remain safe while enjoying uninterrupted service. Proactive fraud prevention measures like SIM-swap monitoring add an extra layer of security for subscribers who might otherwise be targets of account takeovers or identity theft. With ongoing monitoring, you can flag unusual patterns without adding friction, allowing you to effectively balance security and convenience.

But it goes beyond risk mitigation. With a focus on intelligent solutions, you can deliver more personalized experiences across the lifecycle, allowing you to proactively offer your customers more tailored offers and maximize upsell and cross-sell opportunities. And personalizing offers can generate 40% more revenue when compared to telcos that don’t. By carefully analyzing customer data and behavior, you can offer real-time recommendations that align with each subscriber’s unique needs and preferences – and maximize the lifetime value of those subscribers as a result. For example, a customer who travels frequently could be offered a specialized roaming package, while a subscriber who always pays their bill on time could be offered incentives and upgrades for their loyalty. This holistic, end-to-end approach enhances satisfaction, sure, but it also boosts engagement and retention. Customer churn is an ongoing challenge for telcos, with an average churn rate in the industry of 30-35%, but subscribers who receive personalized offers and support are more likely to feel connected, and loyal, to your brand. Focusing on AI-driven personalization enables you to turn routine customer interactions into meaningful engagements, going beyond a traditional provider-customer dynamic.

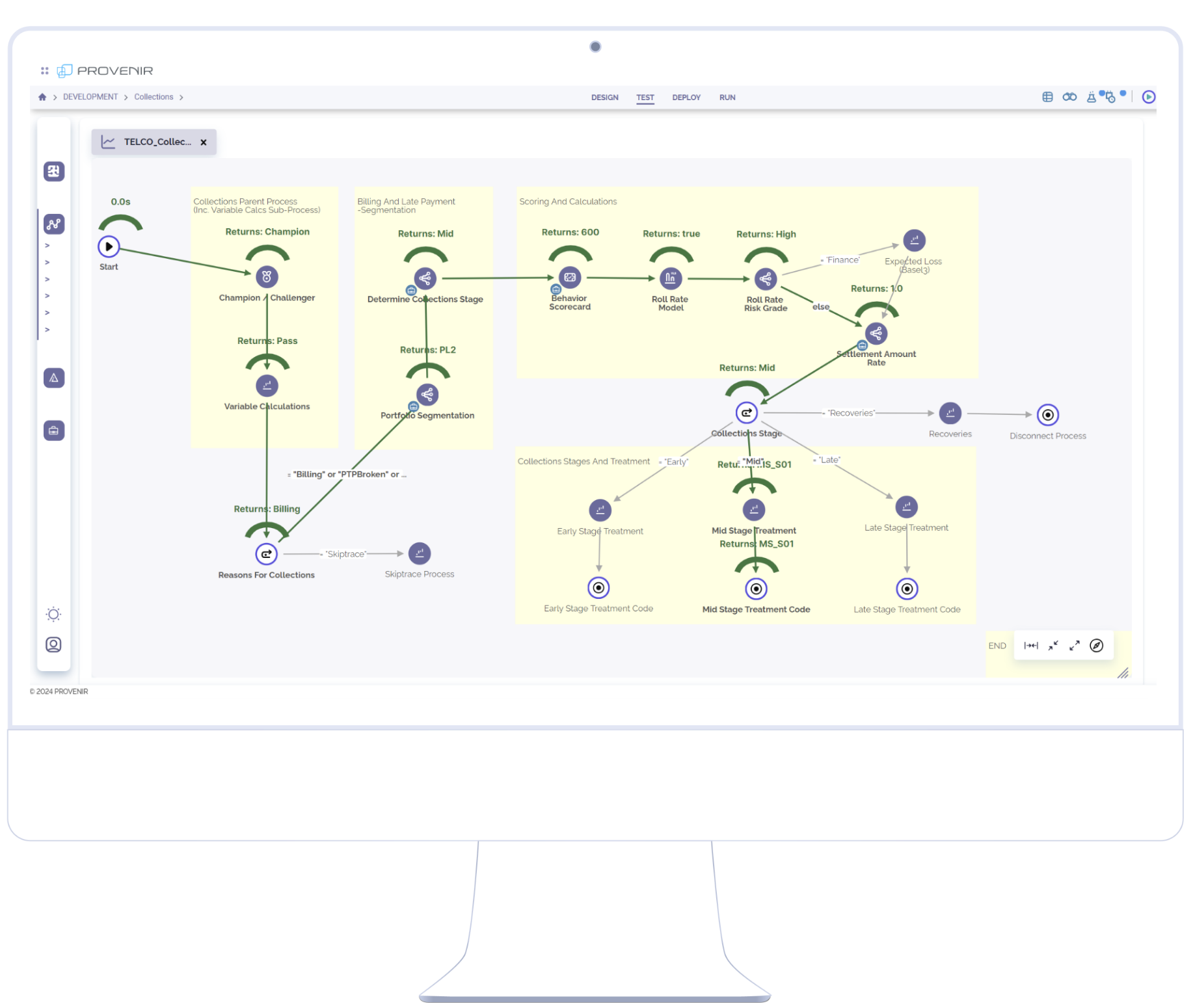

Collections present a unique challenge in the telco industry. Recovering payments is essential for financial stability, but it’s also critical to maintain positive relationships with your subscribers during the process. This balancing act between securing payment and preserving goodwill needs a strategic approach that recognizes the lifetime value of a customer beyond the current transaction. With a heavy-handed or impersonal collections approach, you’re asking for dissatisfaction and churn, underscoring the need for more thoughtful, customer-centric collections practices.

With intelligent decisioning, you can enable collections treatment strategies that consider each subscriber’s unique profile and history. By leveraging data-driven insights, you can create tailored repayment terms that align with unique financial situations, making it easier for your subscribers to meet their obligations without feeling pressure or shame. AI-driven solutions allow you to further segment subscribers based on risk profiles and payment behavior. Low-risk customers who miss a payment as an oversight can be contacted with a gentle reminder via a low-pressure channel, while high-risk customers can receive more proactive, assertive assistance options. By segmenting your subscribers and providing customized communications via preferred channels, you can approach your collections strategy with a focus on preserving relationships (and maximizing the lifetime value of your customers), reducing the chance of churn. And with a transparent, empathetic approach to your collections communications, you’ll further cement those positive relationships.

Delivering an exceptional customer experience across the entire subscriber lifecycle is essential for managing risk, sustaining loyalty, and fostering growth. From onboarding through to ongoing customer management and collections, each stage in the subscriber lifecycle offers you an opportunity to build stronger, more enduring relationships. Embrace automation. Enable personalization. Utilize intelligent decisioning. These strategies will allow you to streamline the customer journey, reduce friction, and provide the tailored experiences your subscribers expect – enabling you to safeguard against fraud and mitigate risk without compromising customer trust.

Investing in innovative, advanced decisioning solutions is no longer optional, it’s a strategic imperative to stay ahead of customer churn – and your competition. By enhancing every aspect of the customer journey, you can ensure your subscribers feel valued and supported, leading to more loyalty, less churn, and sustainable long-term growth. Ready to elevate your approach?