Buy Now, Pay Later (BNPL) has come a long way since it shook up e-commerce at the height of the pandemic. While it was once the poster child for fintech innovation, the backlash against the point-of-sale loans has set in. BNPL providers can no longer afford to acquire customers at any cost – it’s time to shift strategies and pivot to profitability.

Explore how you can future-proof your BNPL technology and build a sustainable strategy that will outlast coming regulation, keep up with changing markets, and reflect economic conditions – all with unshakeable accuracy. Read the eBook to get started!

Read the eBook to discover:

Global BNPL challenges and opportunities

What to expect from upcoming regulation

How to pivot your strategies to become profitable

The future-proof technology you need for sustainable success

Class is in session in this TDS mini, a bite-sized nugget of insight from The Disruptor Sessions!

Provenir’s Head of Client Delivery, Chris Barber, breaks down Buy Now, Pay Later 101. You’ll learn about the imperative for speedy, data-driven technology, how flexibility is essential to get ahead of BNPL’s evolution, and what to focus on for long-term success.

Listen Now

Tune into our Podcast on Apple or Spotify by clicking the icons below.

Apple Podcast

Spotify Podcast

The Panelists:

Chris Barber

Chris Barber leads Professional Services in EMEA for Provenir, a global leader in data and AI-powered decisioning software. In this role, Chris develops strategies and operations resulting in best-in-class services to help customers improve efficiencies and accelerate their business transformation.

Chris brings more than 25 years of global experience in the financial industry actively leading digital transformation projects focused primarily on credit, onboarding, portfolio management, revenue forecasting, loan capital management, regulatory reporting and lifecycle management. Prior to joining Provenir, Chris held senior consulting leadership positions at J.P. Morgan, Schroders and Morgan Stanley. Chris earned an MSci in Astrophysics from University College London.

Chris Barber

Chris Barber leads Professional Services in EMEA for Provenir, a global leader in data and AI-powered decisioning software. In this role, Chris develops strategies and operations resulting in best-in-class services to help customers improve efficiencies and accelerate their business transformation.

Chris brings more than 25 years of global experience in the financial industry actively leading digital transformation projects focused primarily on credit, onboarding, portfolio management, revenue forecasting, loan capital management, regulatory reporting and lifecycle management. Prior to joining Provenir, Chris held senior consulting leadership positions at J.P. Morgan, Schroders and Morgan Stanley. Chris earned an MSci in Astrophysics from University College London.

Provenir to Start Supplying Quick Finans with AI Functionality

Provenir continues to meet the increasing demand for its AI-Powered Data and Decisioning Platform around the globe. This Payment Expert article discusses how Provenir is expanding its global partnerships network in Turkey by partnering with Quick Finans to quickly approve and onboard its new customers.

Quick Finans is one of the multiple international deals Provenir has signed, including DeltaPay, a BNPL provider in Africa aid focused on increasing the financial inclusion rates in Africa.

Merge Ahead – What Happens When Buy Now, Pay Later and the Credit Card Industry Intersect?

Accelerating growth by working together

The BNPL industry, while similar in theory to credit cards, has provided a unique twist on credit – it’s immediate, it’s typically for a single purchase (traditionalBNPL productsdon’t offer an open-ended credit limit) and there is usually a set installment plan for repayments (most often three or four).

But even that is changing – as more BNPL providers enter the growing market space, they are changing the rules (and the products offered) at a rapid pace. As providers and products continue to evolve, the wants and needs of customers are coming sharply into focus – for example, some consumers have expressed frustration at the one-and-done aspect of installment plans at checkout, and would rather have a revolving, renewable credit limit, which certain providers now offer.

BNPL in its current state began as a 21stcentury, usually internet-based alternative to credit cards, allowing consumers to purchase items at point of sale (either online or in a physical store location) via installment plans. Australia is often credited with being the pioneer of BNPL, with giants like AfterPay and OpenPay, but Sweden-based Klarna brought the movement to Europe and other companies began offering BNPL services across the globe in quick succession. As more regulatory oversight comes into play and more widely varied BNPL products emerge on the scene, industry analysts and other providers may increasingly look to how Australian products react to shifts in trends as an indicator for how the evolution of the market will play out globally.

It’s clear the fintech buzz-term of the decade has to be Buy Now, Pay Later – it’s impossible to get away from. But as BNPL continues to grow and evolve so rapidly, where does that leave the credit card industry?

BNPL Crashes Credit Cards’ Party

The impact of the meteoric rise of BNPL has not gone unnoticed by the credit card industry. Consumers, especially the younger generation, have been actively looking for alternatives to high-interest credit cards, forcing traditional lenders to be more competitive if they want to stay relevant. Sixty-two percent of current BNPL customers think that the payment concept could completely replace their credit cards1, with just over a third of users in the U.S. (36%) being repeat customers – utilizing BNPL services once a month or more2. As of April 2021, about 5.8 million Australians have a BNPL account, while 38 percent of people in Singapore utilize BNPL for frequent purchases.3

With BNPL on its rapid ascent, where does that leave credit cards? Since the start of the Covid-19 pandemic, the value of credit card transactions in the United States has dropped by approximately 11%4. You could argue that consumers were spending less thanks to job loss and closed stores amid economic uncertainty, and there may not be definitive data yet to suggest they are shifting spending from credit to BNPL, but datadoessuggest “a universal decline in credit card ownership,” particularly among Gen Z consumers, half of whom don’t even own a credit card4. As the revenue streams of big banks in certain regions dry up thanks to loss of interchange and other card-related fees, the credit card industry is looking for ways to offset those declining transactions. Rather than looking at BNPL as direct competition, banks and other traditional lenders can look at BNPL as an opportunity.

“As the digital word spins faster, people expect financial services to be aligned with their busy and demanding lifestyles. The wide adoption of [BNPL products] being universally integrated into purchases reduces friction, grows sales, and gives consumers more options to improve the customer experience. Banks that ignore this market dynamic risk missing out on the opportunity to engage with future generations of borrowers.”4

Lending United

How can BNPL and credit cards work together then? Is there an ideal future state where each space merges together to offer consumers the best of both worlds? There are pros and cons to traditional credit card lending as well as Buy Now, Pay Later plans – depending on a particular consumer’s perspective, risk comfort level, cash flow needs, credit history, etc. If banks were able to include checkout purchase options in their digitization strategy4, they could help ensure longer-term growth potential – perhaps giving users options to pay in installments via credit card or offering lower interest rates. Some consumers may not be aware that the traditional BNPL model shifts the interest fees away from the consumer and onto the merchant, offering a mutually attractive option for both (less perceived interest on the part of consumers, and larger carts with less abandonment for merchants). But, in part as a result of the apparent lack of interest, some 30% of BNPL users trust BNPL providers more than credit cards when it comes to fair business practices.5

BNPL providers could protect consumers with a blended approach – keeping the simplified lending consumers love (particularly at checkout) but offering additional rewards or perks and ensuring that consumers are able to actually build credit with their use of installment payments. And the rewards of convergence would be worth it as the runway of opportunities is not getting any smaller – a study by Mastercard showed that “43% of consumers in Asia Pacific are willing to increase their spending by at least 15% if allowed to pay in installments.” Meanwhile a research study conducted by Coherent Market Insights showed that the global BNPL market will grow to upwards of $33.6 billion by 2027 (a massive increase from $7.6 billion in 2019)6. To capitalize on this growing market (and those consumers who want to increase their spending) MasterCard invested in Pine Labs, an Asia-based BNPL provider. The partnership aims to bring new installment plans to Asia, with a solution rolled out earlier this year in Thailand and the Philippines, followed by Vietnam, Singapore and Indonesia. Credit, debit and bank cardholders in the region will subsequently have access to installment plans for both online and bricks and mortar merchants upon checkout.

With more than half of the world’s consumer borrowing happening in the Asia Pacific region, there are massive opportunities for fintechs to offer shoppers what they want – namely flexibility and convenience. In a press release from earlier this year, Sandeep Malhotra, Mastercard’s Executive Vice President, Products & Innovation, Asia Pacific outlined the benefits to both consumers and merchants. Flexibility and cash flow management for the former; an increase in sales and reduction in cart abandonment for the latter. And of course, the development of an omni-channel solution benefits MasterCard too: “Installment options complement Mastercard’s wide range of payment programs and align completely with Mastercard’s mission of fostering an integrated, inclusive digital economy and delivering great checkout experiences with payments that are secure, simple and smart.”7

MasterCard isn’t the first credit card company to think outside the box (and they won’t be the last). American Express launched a BNPL-style service in 2017, with its cardholders utilizing installment payment plans for nearly $4 billion in purchases. The “Pay It, Plan It” program directs AMEX to pay a card transaction right after it’s made through a linkage with the consumer’s bank account, and then permits consumers to turn that card transaction into a short-term installment plan for a small fee8. As mentioned, traditionally the merchants pay these types of fees, meaning AMEX is shifting this cost to the consumers – another example of the many ways the term BNPL is no longer a one-size-fits-all product.

By utilizing some of the most-loved aspects of BNPL, credit cards can help ensure their ongoing relevance. And at the same time, evolving their lending methodology andrisk decisioningprocesses could help them widen their net. For example, “alternative data can be used to better underwrite loans for consumers who fall outside of traditional credit metrics,” like the unbanked or underbanked (who usually love BNPL), particularly in regions where it’s very difficult for the average consumer to build credit because spending profiles have changed9. Using technology to better access and aggregate real-time data to make better credit decisions can also potentially provide an easier intersection of BNPL and credit cards – better data and instant decisioning means less risk, allowing providers to offer more personalized payment plans. As Jim Marous put it, “financial institutions must deliver innovative credit options, on-demand, in an almost instantaneous manner” to capture the hearts (and wallets) of their target audience10.

A Match Made in Fintech Heaven

The future of BNPL is here – in fact, it changes almost daily. And the credit card industry can clearly capitalize on that on a wider scale, if the success of the regional, niche partnerships that MasterCard and AMEX offer are any indication. Not only does a thoughtful marriage help both industries continue to benefit from the incredibly large runway of available market share, it helps merchants and consumers too. As we strive for more inclusion in this increasingly global, diverse world, BNPL and credit cards have the opportunity to give more viable lending/payment/purchasing optionsandmore protection to all types of consumers, especially the unbanked and underbanked. And what better way to help stimulate the global economy than being sure that everyone has a chance to participate in it?

For more information on what industry influencers say about the future landscape of BNPL,read our latest eBook.

Fintech DeltaPay Selects Provenir’s AI-Powered Data and Risk Decisioning Platform to Power its Buy Now, Pay Later Offerings

DeltaPay cites Provenir’s flexible architecture, easy access to data and technical expertise as key to providing more citizens with access to affordable credit

Parsippany, NJ — Provenir, a global leader in AI-powered risk decisioning software, announced today that DeltaPay, an emerging fintech headquartered in Kenya, has selected Provenir’s AI-Powered Data and Risk Decisioning Platform to power its Buy Now, Pay Later offerings.

DeltaPay’s mission is to empower people with the financial access to enable them pursue lives of dignity and prosperity. By leveraging alternative data, including behavioral data, DeltaPay provides more citizens with access to affordable and flexible credit. This allows them to improve their purchasing power, and ultimately, their livelihoods.

“Our mission is to provide millions of unbanked and neglected segments with access to affordable credit. In our quest, we sought a like-minded partner to complement our business model and help us scale,” said Kiprop Chirchir, CEO and co-founder, DeltaPay. “Provenir’s architectural design, platform flexibility and technical capabilities set them apart from their competitors.

The Provenir Marketplace provides easy access to financial and behavioral data partners through a single API, which not only makes technical implementation easier but also enables us to go to market faster. Following our launch in Kenya, we plan to scale our operation to other regions including Uganda, Tanzania, Rwanda, DRC, Nigeria and Ghana in the next five years. Provenir will be our partner of choice in this expansion plan.”

“DeltaPay is differentiating itself by creating a holistic view of an individual’s ability to pay through the use of alternative data,” said Adrian Pillay, Vice President, Middle East and Africa for Provenir. “Our AI-Powered Data and Decisioning Platform provides the data, AI and decisioning capabilities needed to help DeltaPay eradicate financial exclusion and improve the customer experience by consistently removing friction from the process for both consumers and merchants. We are excited to partner with them on this journey.”

Provenir’s industry-leading AI-Powered Data and Decisioning Platform ease of use and flexibility allows for smarter risk decisioning. The solution, managed through a single UI, empowers organizations to innovate further and faster than ever before, driving the continuous optimization they need to power growth and agility, without increasing risk.

The Ultimate Guide to Decision Engines

What is a decision engine and how does it help your business processes?

Data Now, Fewer Losses Later: Optimize Your BNPL Data Strategy

Buy Now, Pay Later (BNPL) products have exploded across the globe, offering a new spin to point-of-sale (POS) financing for both consumers and businesses. From 2019 to 2021, BNPL loan originationsincreased by 970%from the top five lenders alone, and the industry continues to expand to include new verticals such as auto repair, grocery purchases, airline ticketing, and more. Consumers are beginning to rely on BNPL for everyday costs in order to help manage their cash flow. But none of this would be possible without data – more specifically, a strong data supply chain.

If you’re a BNPL provider, the data supply chain is the powerhouse for your solution. When you have the right data, you can better determine risk, protecting your business against fraud and loan default.

BNPL data strategies look beyond traditional data like credit scores and use alternative data to make credit more accessible and faster to approve without increasing your risk. While this allows you to expand your customer base in a secure way it also adds complexity to your data needs. So, how do you build a BNPL data supply chain strategy that gets the right data to the right place exactly when you need it?

Building Your BNPL Data Supply Chain

We know every potential BNPL customer must go through a process, but what does that process look like? Each step is built with different data checks that tell your decisioning engine whether to move that customer forward. An optimized data supply chain pulls only the necessary data needed for a customer at each checkpoint – data that comes from your data integrations and data partners.

An optimized data supply chain has these hallmarks:

Multiple steps with distinct requirements

Multiple checkpoints at which consumers either pass or get denied

Steps that increase in complexity and cost of data

No unnecessary data is exposed and paid for before you need it

Launching with an MVP:

Are you a startup launching your first BNPL solution? A finserv expanding your product line? Maybe you’re an online shop looking to reach more customers. Whatever the case, when building a new data supply chain for your BNPL offering or optimizing an existing one, you should begin with your minimum viable product (MVP) – the basics you know you need to launch your product.

An MVP has the least amount of checks in the process, pulling in the least amount of data. You might want to begin with an MVP if you want to:

Go to market quickly

Minimize the cost of development

Analyze basic performance to optimize more complex iterations in the future

To launch with an MVP approach you’re going to need data to support three key areas:

Regulatory compliance checks like KYC/AML

Identity verification

Credit risk

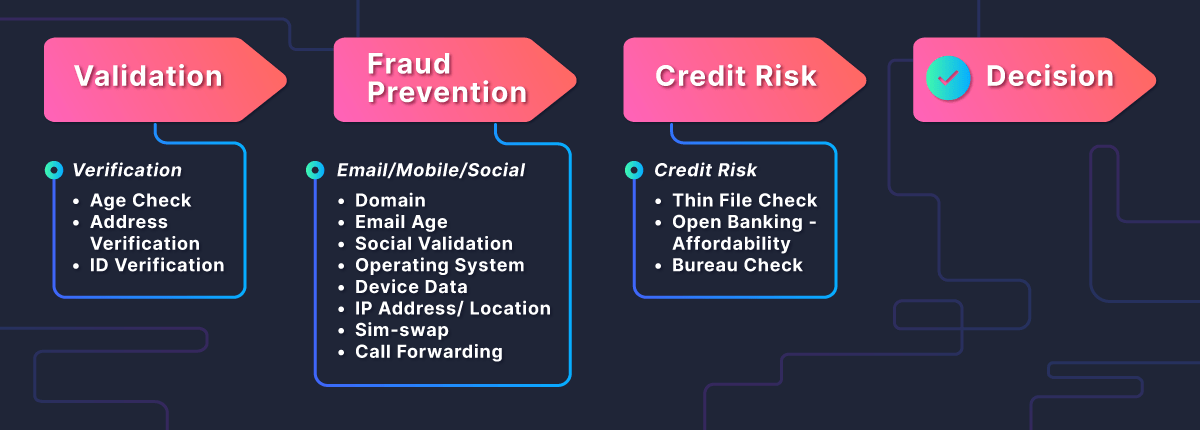

An MVP for consumer lending could look like this:

Step 1: KYC

The first step of the process is validating the most basic data to confirm the customer’s age, address, and identification. If you can’t verify a person’s ID, you certainly can’t lend to them.

Step 2: Fraud Prevention

The second step digs deeper into a person’s identity to ensure they are who they say they are and help prevent fraud. There is a wide variety of data you can pull for a fraud check, including email address verification, if a SIM card has been swapped, and other behavioral and alternative data. If not all of this information matches, it could be a sign of attempted fraud, and the person would be rejected.

Step 3: Credit Risk

The final step is to check creditworthiness. A bureau check is done through a soft credit check that grants you access to a consumer’s credit score without impacting it. With an MVP, BNPL providers would likely reject anyone with a score below a certain threshold or someone without enough credit history to have a score at all. If a person has made it through the process, the data is assessed holistically by a decisioning engine to determine whether and at what terms to grant the loan.

Beyond the MVP: Optimizing Your Data Strategy

Beyond the foundation needed for an MVP launch, you can optimize your supply chain based on your company’s risk appetite and goals. Before updating your data supply chain it will help to:

Analyze success against your goals

Identify weak points in your data strategy

While you may want to initially launch your BNPL solution using an MVP, as you grow and want to add complexity, you can incorporate new data points and data partners. Think about the kind of customer you want to capture, as well as business goals and preventative measures you may want to take, and ask yourself:

What percentage of fraudulent applications is our current process letting through? Is this in line with our business goals? If not, look to:

Add additional fraud checks on existing steps

Add standalone fraud prevention steps to the process

Amend data sources to optimize as you go

Are we offering the most competitive terms to our customers? How can we improve conversions? For competitive edge and increased personalization, use data such as:

Behavioral trends

Geolocation

Activity and usage

How effectively are we reducing defaults? Are we filtering out non-viable customers at the right point in the process? Make sure your flow features:

Prescreening

Scoring

Additional data checkpoints on existing steps

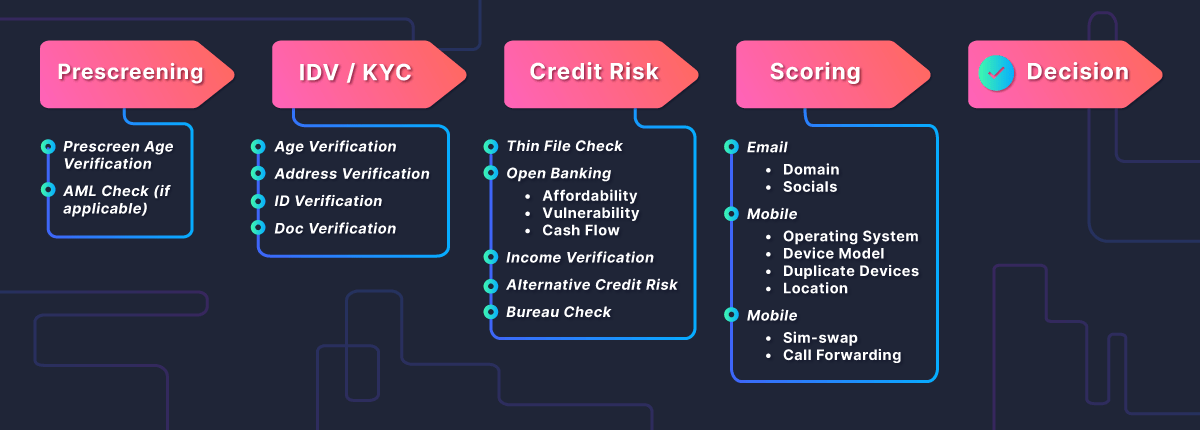

For BNPL providers that want robust data supply chains across credit, identity, and fraud while maximizing efficiency, an optimized flow could look like this:

Prescreening

Prescreening breaks down the identification verification steps even further, making sure the minimum requirements are met. It’s a faster, more efficient way to filter out unqualified applicants without using unnecessary time and resources.

What does prescreening look like in an optimized supply chain? Say you have a person under 18 – they’re not legally allowed to take out a loan, so their application would be rejected. In an MVP, someone that can’t even use the product would still have their identity verified, but it’s a waste to run those checks, since they’re not a viable customer. Optimization ensures you expose only the data you need at each step.

Scoring

Scoring pulls supplementary data that helps paint a clearer picture of a consumer’s risk. This includes mobile device data, additional fraud checks, or any other kind of alternative data you want to feed into your decisioning tech.

Why include scoring in your process? Again, it comes down to building your process for optimal efficiency and minimal cost. At this point, you would know if the customer was viable, who they are, and what their financials look like – this is all straightforward data to pull. Scoring adds behavioral information that is more time-consuming and costly to analyze and should be incorporated only when everything else checks out.

Ultimately, the more relevant data you have, the more accurate your decisions will be, the better you can predict future defaults, the easier it will be to identify upsell and cross-sell opportunities – whatever your business goals, the right data can help you get there. Optimizing your consumer BNPL supply data chain is dependent on finding the ideal number of checks and steps to accurately determine creditworthiness and risk, while keeping the process fast and efficient.

Ready to launch and expand your BNPL products? Look out for these data supply chain challenges

As BNPL products continue to grow around the world, new markets have emerged, and with them new challenges. To build a global supply chain, you have to know regional regulations, vendors, tech requirements, and more. Some of the challenges that can slow down deployment of your data strategy include:

Identifying relevant local data sources

Negotiating multiple contracts

Complying with varying regulations

Ensuring data privacy for different regional requirements

Normalizing data formats

Building and maintaining integrations

Supporting global strategies

BNPL is a fast-moving industry, so it’s also important to ensure your supply chain can be easily iterated on to incorporate evolving legislation and market demand.

Data Powers BNPL

Regardless of trend, customer type, or region, your BNPL solution is powered by data. Diverse data sources pulled at the right time in the right order is the calling card of an optimized data supply chain. And an optimized data supply chain feeds your decisioning engine the information necessary to give you a smarter decision every time.

Building a data supply chain on your own, however, can be a huge undertaking and an even bigger headache. Instead, consider choosing a data partner that can build it for you, while connecting you to the integrations you need to grow your BNPL business.

Ideal features include:

One data contract that gives you access to multiple data sources

A single API to replace numerous integrations

A wide variety of data types and sources, including alternative data

Expert data source curation customized to your needs

Simplified, no-code data supply chains that non-technical users can control

Global data access

Integrates into your decisioning technology to ensure seamless and smarter decisions

Do you want your data on-demand? Meet Provenir Data.

In Asia Pacific, ecommerce sales are skyrocketing and are poised to reach a new milestone of $2 trillion by 2025, a testament to the growth of ecommerce platforms and the shifting consumer behavior from retail to online sales. Along with that, adoption of new payment options, such as BNPL, has quickly expanded. India’s BNPL market stands at $3 to $3.5 billion today but is expected to see a huge surge of up to $45 to $50 billion by 2026. In this article in The Times of India, Varun Bhalla, Country Manager of Provenir, India explains how BNPL can help drive financial inclusion and e-commerce convenience.

The Buy Now, Pay Later market continues to grow and diversify. New providers are still emerging, partnerships between fintechs and larger, traditional banking institutions are solidifying – and consumers are getting more and more demanding. Sixty percent of customers abandon applications for unsecured lending products during digital onboarding, due to slow or complex application processes and a lack of(real or perceived) security. Whether you’re a new entrant to the market or a seasoned BNPL provider, providing a frictionless customer experience is critical to maintaining your competitive advantage. But how can you stay ahead of the competition and still effectively manage your risk?

Key Highlights:

Why a unified platform for data, AI and decisioning can help you analyze and action your data (including decisioning performance data, credit risk, fraud and compliance) for flexibility and scalability throughout the entire customer lifecycle

How easily accessing a variety of data sources(including alternative data) via a single API, offers a more holistic view of your customers, and encourages financial inclusion

The importance of automated decisioning for real-time approvals and a frictionless customer experience

How to develop, deploy and adapt sophisticated risk models without heavy reliance on your vendors/partners – getting you to market faster than your competition

How BNPL Providers can Future Proof Their Technology Platforms

In the fast-moving BNPL sector, risk decisioning that’s accurate and based on real-time information is essential. Equally important is the ability to adapt and comply with a changing regulatory landscape.

In this interview with Nordic Fintech Magazine, Frode Berg, General Manager of EMEA for Provenir, discusses how an AI-powered, purpose-built risk decisioning platform can deliver benefit for BNPL consumers and merchants.

Like a runaway train, Buy Now, Pay Later continues to gather speed in North America. While more providers enter the increasingly attractive (and crowded) market and diversify their offerings, consumers get more and more demanding.

Sixty percent of customers abandon applications for unsecured lending products during digital onboarding, due to slow or complex application processes and a lack of (real or perceived) security. If you’re a BNPL provider, nailing the entire experience is critical.

But how can you get to market faster than the competition, ensure scalability in your product offerings, provide a superior customer experience AND still manage your risk effectively?

They key is in the data and the technology you choose. Hear Kathy Stares, EVP of North America at Provenir, discuss the critical factors to consider when selecting technology partners to grow (or start!) your BNPL business – and how to stay ahead of the competition.

You will learn:

To easily access a variety of data sources (including alternative data) via a single API for a more holistic view of the creditworthiness of your customers

Why a unified platform for data, AI and decisioning can help you analyze and action your data (including decisioning performance data, credit risk, fraud and compliance) for flexibility and scalability throughout the entire customer lifecycle

How to automate decisioning for real-time approvals and a frictionless customer experience

To develop, deploy and adapt sophisticated risk models without heavy reliance on your vendors/partners – getting you to market faster than your competition