Digital Loan Origination in Banking: Competing with Challenger Banks

BLOG

Digital Loan Origination in Banking:

Competing with Challenger Banks

The financial industry has seen a dramatic shift in recent years with the rise of challenger banks. These digital-first establishments have emerged as serious competition to traditional banks, offering more personalized and innovative services that resonate with consumers. To compete with these new players, traditional banks must improve their digital capabilities and offer more streamlined services that provide customers with a better experience.

One area where banks can focus their efforts is digital loan origination. By automating this process and integrating it into their digital platforms, banks can provide customers with faster, more efficient loan processing. This is a crucial component in building a more competitive and innovative financial institution.

Digital loan origination allows banks to gather customer information and evaluate creditworthiness quickly and accurately. By leveraging data analytics and machine learning, banks can make better lending decisions while reducing the risk of defaults. This technology also makes it possible to offer more personalized loan products, which can increase customer satisfaction and loyalty.

Traditional banks can compete by improving their digital capabilities, and digital loan origination is a key area where they can focus their efforts. By automating loan processing and leveraging data analytics and machine learning, banks can make better lending decisions and provide customers with a better experience.

The End of the Level Playing Field

After the 2009 financial crisis, trust in traditional financial institutions took a hard hit with up to 80-90% of the public viewing them as untrustworthy, according to past studies. This led to an opportunity for challenger banks to enter the market with a clean slate and build their brand without the negative sentiment experienced by traditional banks.

Challenger banks also had a technological advantage over their established counterparts. Without the burden of legacy IT systems, challenger banks were able to adopt modern technology and offer digital services with greater efficiency and agility. As a result, challenger banks are quickly gaining ground, and the traditional banks are being forced to adapt or risk being left behind.

Challenger Banks: Reshaping the Future of Banking?

As the banking industry undergoes a transformation, many experts suggest that Challenger Banks will play a significant role in shaping the future of banking and money, despite the challenges that come with innovation. Unlike traditional banks, Challenger Banks tend to embrace a start-up mentality, leveraging a minimum viable product (MVP) approach to continually refine their product portfolio until they achieve the optimal balance.

While larger banks may struggle with operating in product silos and stretching their resources too thinly, Challenger Banks can prioritize quality and customer experience, giving them a competitive edge. But how can traditional banks compete with these innovative newcomers who are leveraging cutting-edge technology and a hyper-focus on innovative products and services?

Also, read: What is Banking as a Service?

Building Consumer Trust in Banking

Traditional financial institutions may have struggled with their reputations post financial crises, but a 2019 survey by Accenture showed extremely positive results for banks when it came to customer trust:

- An average of 77.75% of consumers (across all persona groups) trust banks to care for their long-term financial wellbeing

Results were not so strong for non-traditional financial institutions:

- Only 35.5% of consumers (across all persona groups) trust non-traditional institutions to care for their long-term financial wellbeing

So, while banks may be lagging behind when it comes to technology, they still outperform fintechs and challenger banks when it comes to consumer trust. Financial institutions trying to compete with their challenger competition should bank on the inherent trust that consumers still hold for brick and mortar institutions as a foundation to secure long-term loyalty with customers. Is this an obvious point to make?

Absolutely. But it’s how this trust can be used to build stronger bonds and expand product offerings that offers a huge opportunity for traditional financial institutions.

Dealing with Data: Customer Trust Expands Opportunities

In a time when data breaches are common, billions of records were stolen in 2018 alone, consumers are on high alert when it comes to sharing their information.

So perhaps one of the most fascinating results of Accenture’s study is that customer trust in traditional financial institutions extends to trusting banks to keep their data secure. 80% of consumers surveyed trusted their banks enough to share additional data to receive more relevant offers.

This gives banks an incredible opportunity to create truly personalized services using data gleaned directly from customers. But banks can go further, with many consumers sticking with the same financial institution for many years, banks have been gathering an immense amount of data on customers that can be used to personalize and pre-approve offers for individuals.

Wouldn’t it be nice if your customer’s felt like you truly understood their needs by offering the right products at the right times?

As a bank there’s a lot that can be learned from how challenger banks have approached disrupting the industry. Let’s consider a standard financial category that you may offer, and how the use of technology and data can improve that experience for your customers.

Mobile Loan Origination

Customers have an increasingly strong preference for the loan origination process to be mobile-friendly and fast.

- Accenture found that on average 81% of consumers would share more information to get faster services and approvals

Challenger banks have greatly improved the loan origination process for consumers. They’ve removed the once long, paper-filled process and made approvals almost instant – all the while accepting nothing less than improved compliance and mitigated risk.

The smart pairing of data access and automation powers much of this process. And, while the idea of a loan being commenced and approved during an afternoon at work would be laughable 20-30 years ago, now it’s expected.

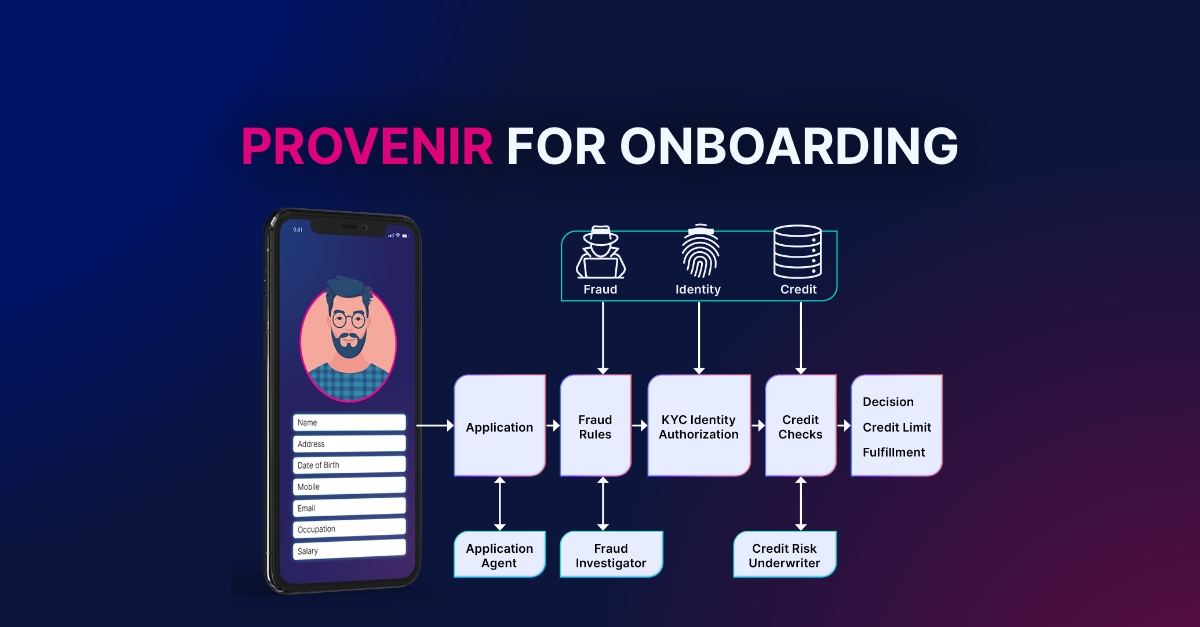

Offering this type of capability can seem daunting for both a startup with 25 employees and traditional banks, but launching a mobile or web app that can collect your customer’s application details, integrates with your systems and third-party data sources, decisions that loan, and provides an approval instantly is only a matter of starting with the right technology.

Building Data into Your Loan Origination Process: Using Data to Level the Playing Field

A common challenge banks face is being able to access, orchestrate, and use data. To get the most out of their historical data and gain access to new data, banks need to find a way to draw their data into one location as a foundation for decisioning and customer personalization.

Connecting disparate systems and data silos can provide banks with a huge advantage over their competitors as they’re able to gain much deeper insights into their customers and more easily assess associated risk. But legacy technology makes this almost impossible in many organizations.

To solve these issues, banks need to look for a solution that allows them to create a decisioning ecosystem. Technology that connects the dots between their CRM, historical data, new customer data, and their loan origination processes.

It’s only by using data to predict customer needs, pre-approve products, and personalize offerings that banks will compete with the challenger banks nipping at their heels. And, if banks can match this personalization across both physical and digital channels, banks could well disrupt the disrupters!

“Our entire approach is built on simplifying banking. One of the ways we do this is by making the customer experience fast and effortless; from the initial on-boarding process through to every subsequent interaction. The Provenir Platform gives us speed and flexibility in our lending operations, which enables a customer to apply for a loan at lunchtime, receive immediate approval, and have the money available in their account later that day.”

– CEO, Instabank

Deliver compliant, personalized digital banking experiences while keeping risk low with intelligent decisioning.

LATEST BLOGS

Beyond Data: Why Dec...

LATAM Next Complianc...

The Architecture Gap...