The State of AI, Risk, and Fraud in Financial Services

The State of AI, Risk, and Fraud in Financial Services

The financial services industry is facing an inflection point. In 2025 (and beyond), staying ahead isn’t just about managing credit risk and preventing fraud – it’s about leveraging AI, unifying data, and modernizing decisioning systems to unlock new growth opportunities.

To better understand the challenges and priorities shaping the industry worldwide, we surveyed nearly 200 key decision-makers among financial services providers globally. The results highlight a pressing need for AI-driven insights, better data orchestration, and an end to fragmented decisioning strategies. This blog breaks down the key takeaways from the survey results and what they mean for the future of decisioning and your business.

Credit Risk and Fraud Prevention:

The Industry’s Top Concerns

The ability to manage credit risk and prevent fraud effectively remains a top priority, especially in an increasingly complex, digital economy. Forty-nine percent of our respondents identified managing credit risk as their biggest issue, and 48% cited detecting and preventing fraud as a primary concern, a noticeable increase from last year’s survey (43%).

While these issues aren’t new, their growing intensity underscores the fact that traditional approaches to risk decisioning just aren’t sufficient any more. Financial services providers are facing more sophisticated fraud threats, rising economic uncertainty, and increasing regulatory scrutiny – making real-time, AI-driven decisioning more critical than ever.

The escalation of fraud in particular is not shocking. While the industry leverages AI and automation for smarter decisioning, fraudsters are also utilizing advanced tech for more complex schemes, creating a never-ending loop. Identity fraud, deepfake technology, synthetic identities, and account takeovers are evolving – quickly. But at the same time, demanding consumers are pushing for seamless digital experiences, with instant approvals and frictionless onboarding becoming the bare minimum. This sort of demand creates a delicate balancing act – how do you ensure the proper security without adding unnecessary friction to the customer journey?

Providers relying on rule-based fraud detection alone will struggle to keep up. Fraud patterns shift in real-time, and static rules can’t adapt quickly enough. This showcases the urgent need for AI-powered fraud prevention solutions that can analyze behavioral data, detect anomalies, and predict fraud with greater accuracy. And AI-powered fraud detection doesn’t just stop fraud – it can also help reduce false positives, ensuring that legitimate customers aren’t caught in security roadblocks.

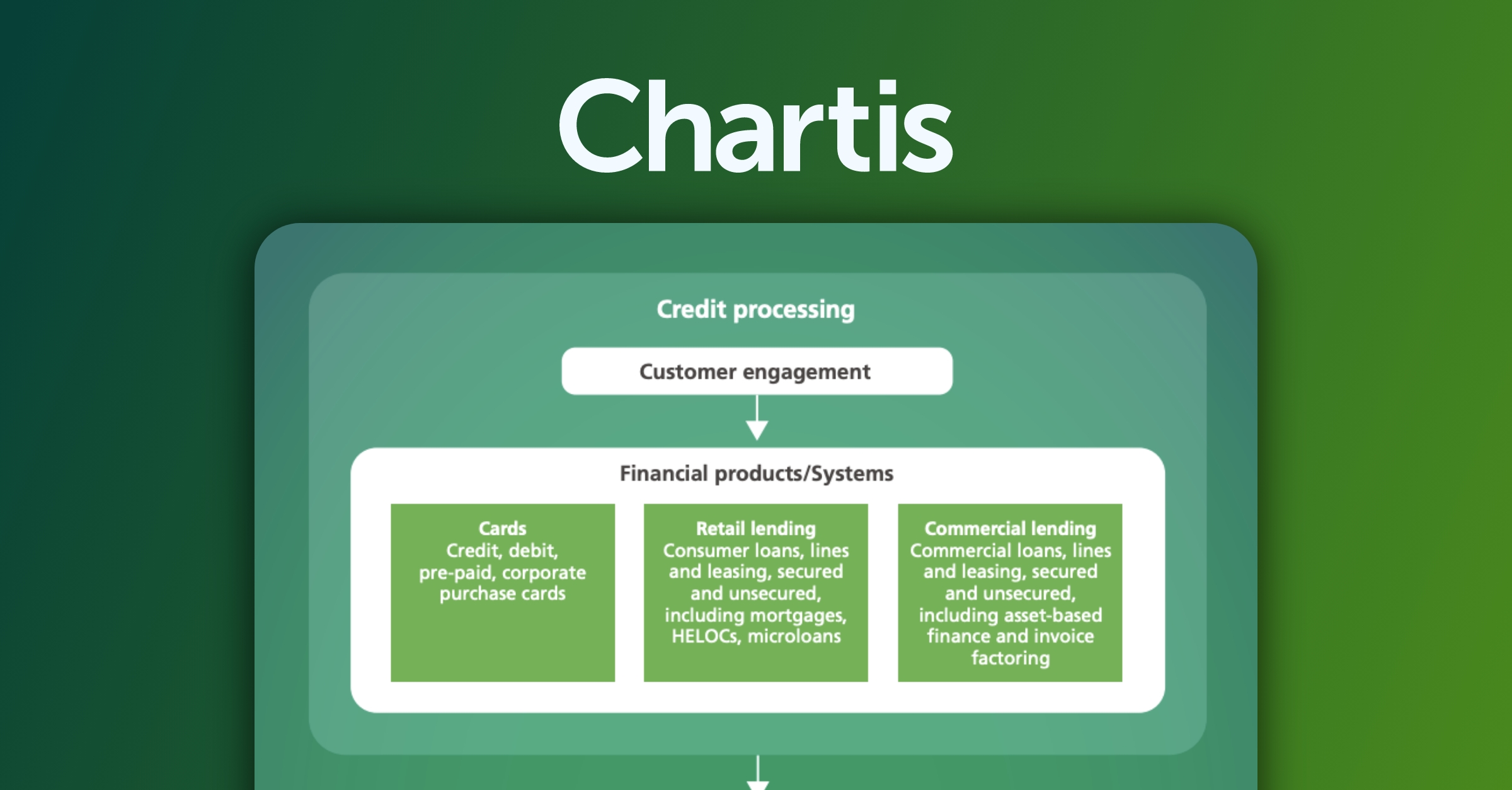

On the other side of the coin, managing credit risk has always been central to financial services providers. But economic volatility, including rising interest rates, inflation concerns, and shifting regulatory policies, means lenders must be more accurate than ever when assessing creditworthiness. Traditional credit scoring models often fail to provide a complete picture of a borrower’s risk profile, and without real-time insights, you may be missing out on prime opportunities for upsell/cross-sell and other revenue gains across the customer lifecycle. Not to mention the very real, very present risk of delinquencies and credit losses.

Over 30% of respondents in our survey cited limited data access as a challenge in risk

decisioning. Without access to real-time financial data, alternative credit signals, and behavioral analytics, making inaccurate credit decisions could either expose you to bad debt or cause you to reject creditworthy customers. Or both.

The Need for a Holistic Approach:

Moving Beyond Reactive Risk Management

Real-time AI-powered decisioning:

Instead of relying on static models, consider AI-driven models that continuously learn and adapt to new fraud patterns and credit risks.Integrated fraud and credit risk teams:

Fraud and credit risk are often managed in separate silos, leading to inefficiencies and missed insights. A unified decisioning approach enables better risk assessment, faster response times, and enhanced customer experiences.Expanding data access and alternative data integration:

The ability to incorporate real-time transactional data, open banking insights, and behavioral analytics is critical for both fraud prevention and credit risk assessment.

Real-time AI-powered decisioning:

Instead of relying on static models, consider AI-driven models that continuously learn and adapt to new fraud patterns and credit risks.Integrated fraud and credit risk teams:

Fraud and credit risk are often managed in separate silos, leading to inefficiencies and missed insights. A unified decisioning approach enables better risk assessment, faster response times, and enhanced customer experiences.Expanding data access and alternative data integration:

The ability to incorporate real-time transactional data, open banking insights, and behavioral analytics is critical for both fraud prevention and credit risk assessment.

The Urgent Need for AI:

Investment Priorities in 2025 and Beyond

- 52%Risk decisioning solutions

- 42%New data sources and orchestration

- 33%Integrated fraud and decisioning solutions

The growing emphasis on AI decisioning reflects a shift from reactive risk management to proactive, real-time decisioning. Financial services providers recognize that AI can enhance credit risk assessments, strengthen fraud detection, and improve operational efficiency—but only if it’s powered by high-quality, integrated data.

While AI adoption is accelerating, poor data integration remains a significant barrier. Without seamless data orchestration, AI models risk being ineffective, leading to missed opportunities and inaccurate decisioning. If you’re investing in AI, you must prioritize data quality and accessibility to ensure these solutions deliver measurable impact.

In 2025, success in AI-driven risk decisioning (and maximizing ROI in AI investments) will depend on not just adopting AI, but implementing it with the right data strategy — one that fuels better insights, faster decisions, and a more seamless customer experience.

The AI Hurdles:

Why Adoption Isn’t as Simple as It Sounds

- 52%Data quality and availability

- 48%Initial costs and unclear ROI

- 47%Integration challenges

- 42%Infrastructure requirements

- 40%Regulatory compliance concerns

Implementing AI requires a solid foundation of clean, integrated data, robust infrastructure, and clear governance. The significant data challenge highlights the need for the seamless orchestration of new and alternative data sources (which can be easily integrated into decisioning) to truly unlock AI’s full potential.

One way to ensure success is to start small and scale smartly. To mitigate risk and ensure measurable impact, consider starting with AI projects that offer quick ROI (credit scoring, automated customer decisioning) or may be slightly less regulated (fraud detection). Try a phased approach, focused on early wins, continuous optimization, and scalable infrastructure, in order to build confidence in AI-driven strategies while demonstrating tangible business value.

Breaking Down Silos:

The Shift Towards Unified Decisioning

- 52%Operational inefficiencies

- 40%Added costs

- 35%Disparate, siloed technology

Slower risk assessments, challenging fraud detection and inconsistent customer experiences are other outcomes from operational inefficiencies – when risk, fraud, and credit teams operate in silos, financial institutions miss out on better collaboration, faster approvals, more accurate risk mitigation, and growth opportunities.

But by consolidating risk decisioning into a single, end-to-end platform, you can:

- Improve cross-team collaboration between fraud, credit risk, and compliance teams

- Enable real-time, AI decisioning for faster and more accurate risk assessments

- Enhance the customer experience by reducing friction and improving approval times

- Maximize value across the customer lifecycle

- Optimize growth for long-term success

Real-Time Decisioning and Personalization:

The New Frontier

- 44%Eliminating friction across the customer lifecycle

- 44%Increasing customer lifetime value

- 36%Hyper-personalization

Traditional, batch-based decisioning models aren’t enough in an era where customer expectations are shaped by instant approvals and personalized digital interactions. AI-driven decisioning can improve risk assessments, but also enables proactive engagement and tailored offers that drive loyalty and maximize customer value.

To meet evolving consumer demands, adopt real-time, AI-powered decisioning models that ensure a more customer-centric approach, and which can:

- Adapt dynamically to customer behavior in real time

- Eliminate unnecessary friction while maintaining strong risk controls

- Leverage hyper-personalization to increase engagement and lifetime value

A Call to Action for Financial Institutions

Invest in unified decisioning platforms

to eliminate silos, reduce inefficiencies, and improve risk assessment accuracyLeverage AI strategically

by focusing on solutions that offer clear ROI and operational impactPrioritize data integration and quality,

ensuring seamless orchestration of diverse data sources to power more intelligent decisioning

The future of risk decisioning isn’t about isolated fixes—it’s about a holistic, AI-powered approach that aligns data, automation, and decisioning processes to maximize impact. Those that embrace this transformation will be better positioned to mitigate risks, drive growth, and deliver superior customer experiences.

Check out the full survey report for detailed responses.