Unlock the secret to smarter credit risk decisioning.

Discover Provenir’s AI-powered, intelligent risk decisions.

From startup to decacorn: credit decisioning software to fit your needs.

Decisioning software isn’t one-size-fits-all. You need purpose-built technology designed to outpace market evolution, and maintain your rank as an innovative and disruptive financial services player. Provenir powers data orchestration and risk decisioning processes across identity, credit and fraud to help you get ahead, and stay ahead of risk. We’ve designed our AI-Powered Data and Decisioning Platform, with key data, AI and risk decisioning capabilities, to give you the flexibility to iterate, expand, and scale on your timeline. Technology shouldn’t dictate your path forward, it should empower it. Define your own journey with a flexible Software-as-a-Service solution!

Banking

To compete in today’s digital-first world, you need to offer innovative banking products, fast approvals, and a world-class consumer experience. But legacy decisioning technology – siloed data sources, disparate software systems, reliance on numerous vendors – can make this difficult for banks, if not impossible.

Customer Management

Making an initial decision at onboarding is only one piece of the customer journey. Discover how Provenir’s AI-Powered Decisioning Platform goes beyond – to enable holistic risk decisioning across credit, fraud, and compliance in order to maximize upsell and cross-sell opportunities, proactively manage and mitigate risk at all stages of the lifecycle, and optimize collections strategies.

SME Lending

Small businesses are the lifeblood of the economy — yet big banks only approve 27% of small business loans. As an SME lender stepping up to increase approvals, you need the right data and a credit risk decisioning platform that helps you understand risk and get SMEs money when they need it.

Buy Now Pay Later

You need to compete in an evolving and rapidly growing market, without increasing risk. Need an alternative to credit risk decisioning with traditional credit scores? We’ve got you covered. Use Provenir’s simple alternative data integration tools, advanced automation, and powerful ML capabilities to onboard and decision merchants and consumers at record speed.

Digital Merchant Onboarding

You want world-class digital merchant onboarding. But strict compliance regulations and evolving fraud risks threaten to slow you down. Provenir’s data and risk decisioning platform simplifies your ability to create, adjust and implement risk processes — powering fully automated onboarding.

Auto Financing

As an auto lender, you need smooth loan approvals that quickly move cars off the lot. Provenir lets you deploy sophisticated data strategies and risk decisioning models to make the right credit decisions in milliseconds without relying on external vendor or dev teams.

Loan Origination

Traditional loan origination software limits your ability to deliver fast approvals and unforgettable consumer experiences. Provenir flips the script, automating end-to-end lending processes. We make data access simple, powering real-time credit risk decisioning in under a second.

Retail + Point-of-Sale

As a retail or POS lender, two things matter: making the right credit decisions, and having the data to make them quickly. Tapping into advanced data science tools, Provenir enables one-click, real-time risk decisioning engine functionalities to power more accurate credit risk decisioning.

Consumer Lending

Consumer lenders must provide fast approvals and simplified processes to reduce abandonment and improve customer experience and competitive advantage amidst evolving regulation. Provenir enables quick approvals, personalized pricing and rapid innovation for a superior customer experience for any use case.

Fintech

Fast, frictionless service is essential for every fintech. You need a platform that empowers you to maintain high levels of service, even as your business grows from innovative startup to industry disruptor. Say hello to Provenir, the premier data and credit decisioning software for the world’s leading fintechs.

Telco

Telcos face intense competition, increased fraud, and high customer churn, making it hard to expand your business to new, creditworthy subscribers. Provenir’s global data platform and smart credit decisioning software can help you increase activations and retain subscribers without exposing yourself to more risk.

Unleash the power of automated decisioning, real-time data and advanced analytics.

PRODUCTS

From data to AI-driven credit risk decisions, we’re powering innovation.

In a digital-first market, agility and innovation are key. The Provenir AI-Powered Risk Decisioning Platform blows past traditional credit decisioning software by letting you harness the power of data, AI and decisioning from one unified, low-code user interface. Whether you’re launching a startup, or scaling a unicorn, Provenir helps you power beyond your business goals. Use Provenir to power one or both of your data and risk decisioning strategies.

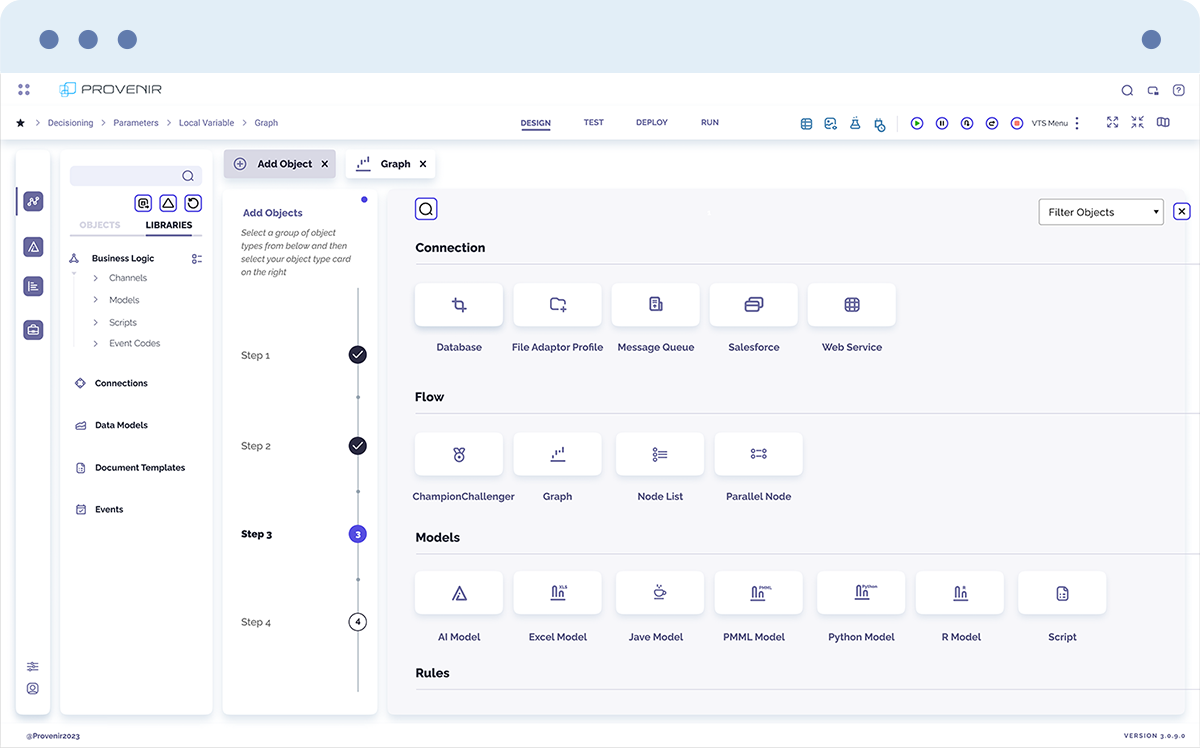

Provenir Decisioning

Provenir Decisioning: Provenir’s industry-leading credit risk decisioning platform lets you make smarter decisions, faster. Use Provenir’s low-code decisioning engine to tackle virtually any risk decisioning or analytics workflow. Empower business users to design, build and deploy new workflows or make changes quickly. Get products to market, today.

Use Provenir Decisioning to:

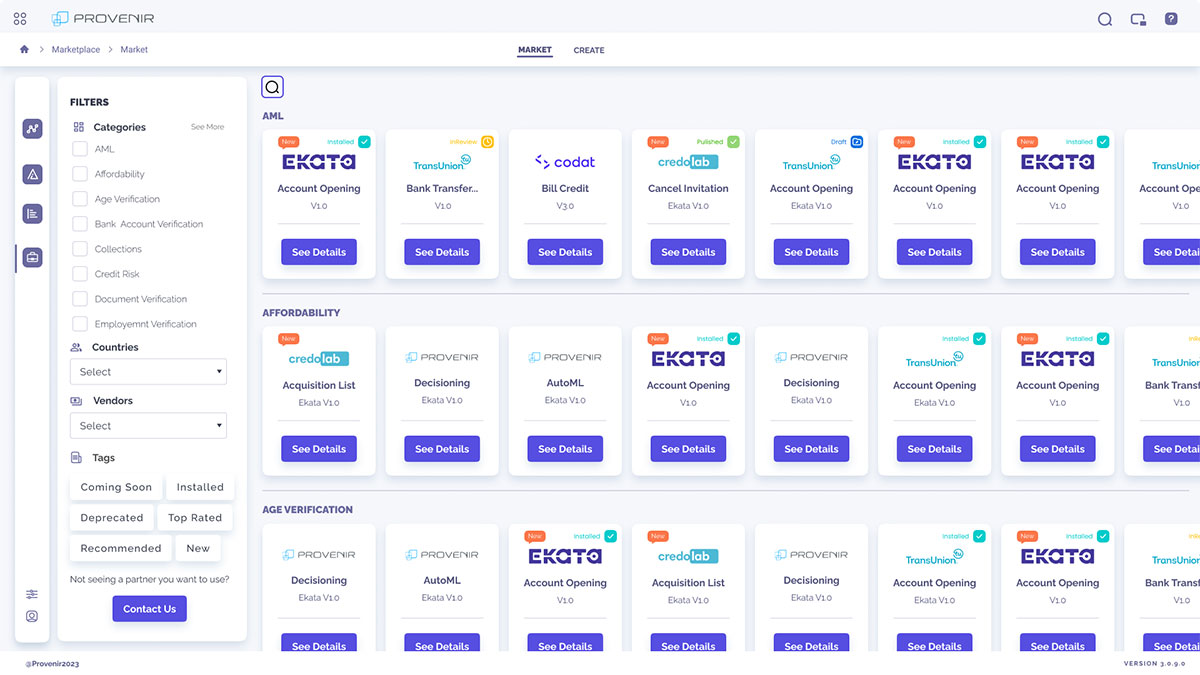

Provenir Data

Say hello to data. Any data, anywhere, on-demand – One API. Provenir Data + Marketplace is a global data and intelligence platform that makes accessing data fast and easy. Advance and accelerate your data strategy with data and insights covering identity, fraud, and credit, all managed through a single contract. Eliminate your data sourcing challenges and simplify your data supply chain with preconfigured, fully maintained integrations, accessed through a single API. Select from identity, fraud, open banking, bureau, alternative sources and more.

Use Provenir Data to:

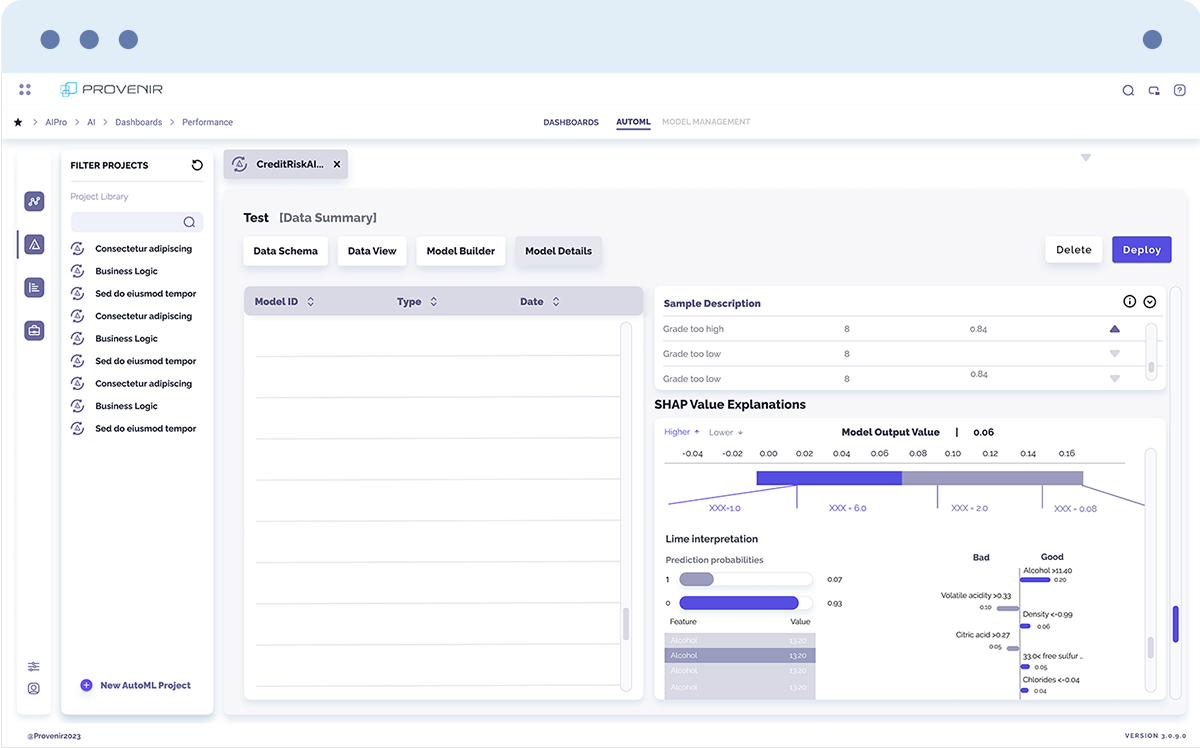

Provenir AI

Simplified AI for smarter decisioning. Designed and built to make AI accessible to fintechs, Provenir AI empowers you to launch your AI strategy at record speed. Whether you’re just starting with AI or are further on your journey, Provenir’s AI solution will bring instant value to your team by eliminating the challenges that limit AI impact. With auto-selection, simplified deployment, and self-optimization, Provenir AI lets you run at maximum performance, all of the time!

Use Provenir AI to:

A recognized industry leader

BENEFITS

Cloud technology that powers risk strategy innovation.

Provenir does more than help with your current tech challenges. We eliminate them.

Designed and built to power agility, our cloud-native technology puts your team in control. Independence replaces vendor-reliance. Seamless support for business growth replaces unscalable technology. And advanced risk decisioning, data and AI capabilities replace aging solutions.

It’s the closest you can come to custom technology without building it yourself.

Built for the cloud, the Provenir AI-Powered Risk Decisioning Platform is an entirely cloud-native platform that considers agility, affordability, flexibility and security as must-haves, not nice-to-haves.

Decision engine success shouldn’t rest in vendors’ hands. Provenir’s low-code cloud platform features a user-centric drag and drop interface, putting your team in charge of uploading, testing, and deploying models and risk decisioning workflows.

A software-as-a-service model, Provenir allows you to develop, QA and deploy your risk decisioning environment on constantly advancing technology. With four product releases per year, we keep our credit risk decisioning software cutting edge to empower your team to focus on strategy.

Data and credit decisioning software that will change the way you think about your risk strategy..

Companies like you use Provenir

GM Financial

GM Financial wanted to bring new auto lending and leasing products to market more quickly, paving the road for smoother loan origination processes. Provenir was there to help.

Klarna

BNPL provider Klarna needed to replace legacy technology with real-time risk decisioning and business analytics designed to keep up with shopper demand. Provenir provided the framework to get there.

SoFi

SoFi benchmarked the project alongside its previous DevOps effort with its in-school college loan application. As a result of building out new automation and leveraging low code/no code technology enabled processes via the Provenir platform, SoFi was able to complete the project and go live in a shorter timeframe (within 10 weeks).

Bigbank

Bigbank needed better credit and lending products that led to better customer experiences. That meant leaving outdated technology behind for a unified platform. That’s where Provenir came in.